Practical Tips to Build an Emergency Fund

This post may contain affiliate links. We may earn a commission if you purchase via our links. See the disclosure page for more info.

Practical, everyday tips to help you build your emergency fund, even when your wallet is empty and you’re broke. It can be done with a little perseverance with these handy tips.

Finding ways to build your emergency fund when you’re absolutely broke seems the most daunting task when you begin your journey to being debt-free. All you can think about is how you’re going to pay the next bill, how you’ll put food on the table, how you’ll put gas in the car. Having extra money to stick aside for a rainy day when you’re living in the thunderstorm now just seems ridiculously foreign when you can’t even pay your next bill.

And telling you to move to a less expensive area or to sell a car is an impractical solution to many of us if we aren’t in a position to make those kinds of sacrifices. The following tips may be common sense to many who are already living a thrifty lifestyle, but if you find yourself needing to create an emergency fund from scratch as you become more purposeful about your life and not just your pantry, these tips can help get you started.

Practical Ways to Build an Emergency Savings

There are practical ways to build an emergency fund penny by penny until you hit your first goal. If you have to dip into that emergency fund occasionally for a real emergency, then you can be thankful that you’ve got it there instead of taking on even more debt load in order to meet that emergency need.

Of course, the basics of creating any kind of savings are:

- Reduce bills – try to work out deals with creditors for lower interest rates, pay your debt in a snowball fashion to get the most out of payments every month, restructure your mortgage if it makes financial sense, downgrade phone plans, get rid of cable, etc.

- Stop spending – frivolous spending eats away at our ability to save and to get out of debt. Trim it wherever possible.

- Increase income — take on overtime, get a second job, find an online job, take a babysitting gig, etc.

But wait, there’s even more!

Many of us have done those things and still find it hard to put anything into a nest egg. This is where we can begin to look for other practical ways to increase your emergency fund without being extreme.

Reduce

Bills will be defined as those ‘needs’ that are month to month. Utilities, prescriptions, food, etc. These are generally non-negotiable for us as far as doing without, but can be changed in terms of how much money goes out on them each month.

• Negotiate better rates on your credit cards. If you’ve been paying on time, and have generally improved your credit rating, you may be able to negotiate more favorable terms with your credit card company, which means you’ll be paying less. You might want to consider NOT paying extra on your cards for a brief time. I share more on that here.

• Negotiate better rates on your utilities. You can call phone companies, cable companies, electric companies, and other utilities to see if updates to packages have been made that might get you a better deal, which means more money in your wallet.

• Refinance your home. If you are paying upwards of 6+% interest on your home, you might consider talking to your lender about refinancing to a better rate. You can shorten the length of your mortgage, decrease your monthly payments, and have more money in your wallet. Be aware of refinancing fees and closing costs, but do some research to see if this can help you in the short AND long term.

Understand that this is NOT a second mortgage. This is simply changing the terms of your original mortgage and converting it to a lower-interest, shorter-term mortgage.

• Eat from your pantry. If you have a decently stocked pantry/fridge/freezer, meal plan to eat from it. Being purposeful in your choices, you can use that pantry as a short-term emergency situation and save that grocery money to put into your emergency fund. Once you’ve built it up with all of the other methods, you can go back and begin building your pantry back up.

• Shop around for better insurance rates. Shop around for insurance rates for your car, home, and health. If you find great rates, contact your current insurer to see if they can match those rates. Be very aware of changes in coverage, deductibles, etc.

• Increase your deductibles. This seems counter-intuitive, but increasing your deductible (meaning you’ll have to pay more out of pocket if you make a claim) is one way to bring home more money every month on home and auto insurance. You can tuck that money into your emergency fund, which will build and help you cover that higher deductible if ever you need to make a claim.

• Downgrade your phone plan. Now that wifi is becoming more widely available, consider temporarily downgrading your phone’s data plan to save $10-50 per month. You’ll need to be mindful of mindlessly scrolling through Instagram or uploading video to Facebook or scrolling through Pinterest while you are at a traffic light.

• Change where you get your prescriptions. Move from one location to another and take advantage of transfer bonuses, or even cost.

Stop Spending Money

Our spending habits are typically that – habits. We habitually spend money on things that are not necessary, but ‘feel’ necessary because we are so used to doing them. Whenever we need to really pinch our money belt tightly, these are the first things we do to help free up some cash.

And while offering advice to stop spending money seems trite, you’d be surprised at how much of your money goes to frivolous spending on entertainment and food for the heck of it. Not things for the groceries or needs, but on things you quickly purchase and don’t even think twice.

- Have family game nights. For this short season, stop going out to the movies (It costs my family upwards of $50 to see a movie in our area if I don’t bargain shop for tickets), cancel your cable, and don’t go out to eat. Stay in, have family game nights, listen to online radio presentations from yesteryear (my kids have always LOVED listening to old radio programs), and watch Youtube. Invite friends over to enjoy the evening with you.

- Stop subscription plans. Many times, we sign up for subscription plans and then never actually use them, or not use them to their full advantage. If you are still subscribing to magazines, online music plans, monthly maintenance plans,

- Stop Consumable Expenses. I’m gonna say it here – stop smoking, stop daily Starbucks runs, stop going out for happy hour, stop going out to party on the weekends. Those activities are hard on your pocketbook AND on your health. This doesn’t mean you have to do without fun forever, but in the short-term, as you build your emergency fund, cut back on everything you can to build it faster. You might just find you don’t miss those things after all – or can live with making them an occasional treat instead of a constant habit.

- Cut back on grooming. This doesn’t mean becoming a caveman or cavewoman in the interim, but if you can stretch haircuts out a week or two, and hold off on manicures every week, you can tuck away that excess, and build your emergency fund faster.

- Cancel warehouse memberships. Costco, Sams, and BJ’s are great for helping us spend money on items we REALLY don’t need. A practical way is to just not visit for a little while if you don’t need to. But if it means canceling a membership to be extreme, then that may be the solution for you.

- Pack your own lunch. I know, I know. Those of us on tighter budgets probably already do this. When lunch costs between $6-9 per day at a fast food restaurant, a day here and there doesn’t seem to mean a lot. But if you eat out more than 2 times per week because it seems easier and faster, imagine the money you’re spending that could go directly into your emergency fund.

- Stop upgrading. Just because style and marketing gurus tell you the new thing is what you HAVE to have, resist that urge. Really – if you thought you were going to upgrade to the new phone, consider NOT doing it and pocketing the difference. Your old phone will probably last another year or two. We’re so habitual in our need to upgrade simply to upgrade, that we end up spending money we didn’t need or have in order to have something that the shine wears off of in just a few days.

- Get thrifty. Sometimes you have to spend. But instead of going straight to retail, look at alternatives such as Facebook Marketplace, Craigs List, area resale shops, garage sales, and swap meets (Mom swap meets are great when you can swap clothes for kids as they go through growing stages instead of buying), etc. While this is more of stretching your budget issue than anything, if you’re in a place where you can put the savings away somewhere else, even for a short time, that’s the way to go!

Increase Income

- Take on a part-time job – even if is only for two months, make that two months count and put that money into your EF.

- Do handyman jobs in your neighborhood like lawn mowing or house cleaning or pet sitting or painting

- Get an online job. There are so many ways to legitimately earn money online (such as virtual assistants, medical transcription, editors, teaching English to foreign students), that you might be able to find something you’re an expert at and help someone else!

- Cashback rewards – obviously, this initially means spending, but if you can get cash back on those things you have to spend money on, you’re putting money back into your wallet. Only do this, though, if you have the stamina not to use a credit card unwisely. We make upwards of $162 a month by putting ALL of our bills and spending onto a cashback card, then paying off once a week and never carrying a balance.

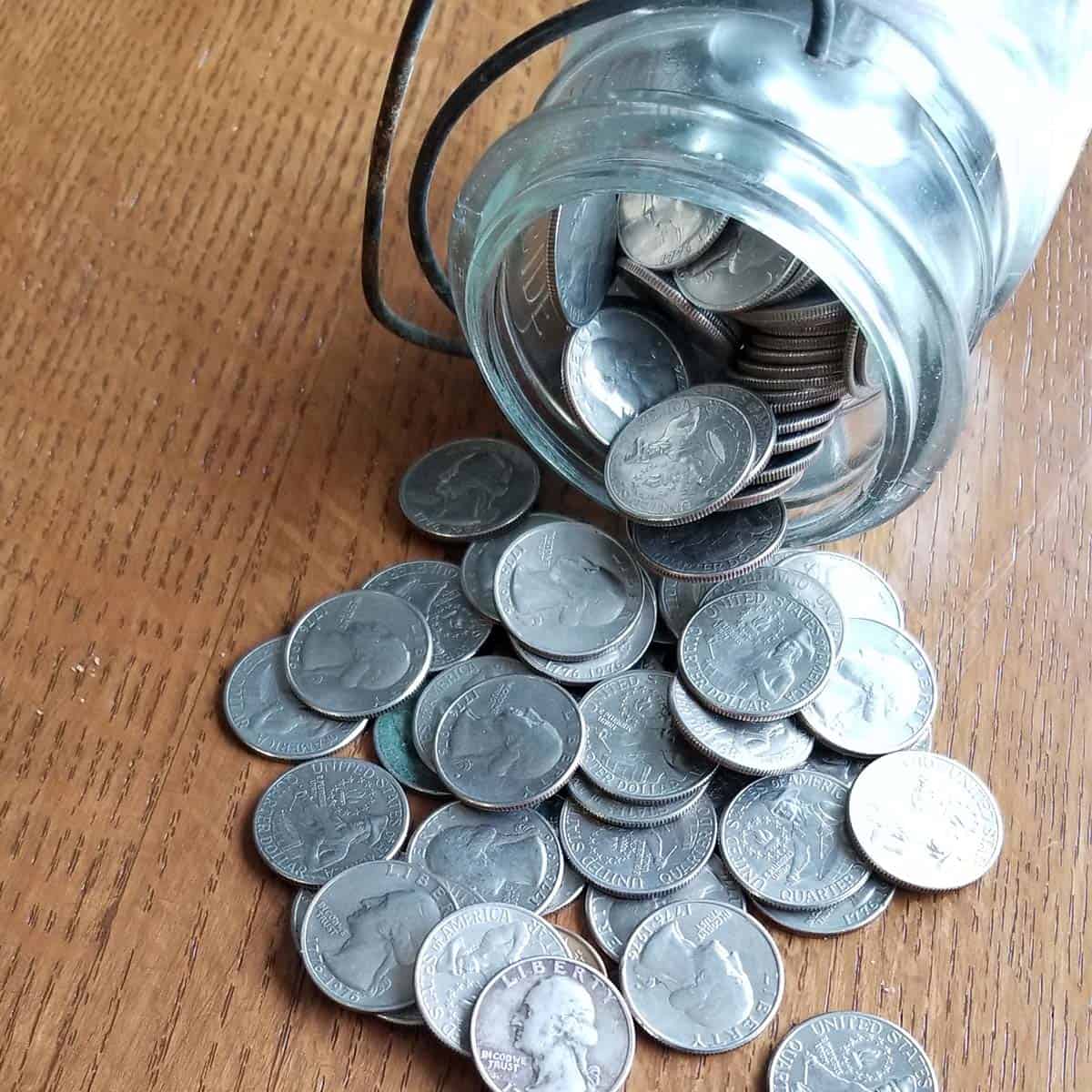

Laundry Tax

Money from the dryer? Toss it into your rainy fund jar. I keep a jar for the coins and occasional bills I find floating in the laundry. Not only does it help increase your emergency fund, but it also helps encourage children to be more mindful of their money.

Of course, if someone loses a substantial amount in the laundry, it’s your choice on what to do with it.

Pick up those coins!

Have you seen that woman walking through a parking lot, stopping, and picking up a coin? That was probably me. Even if you are picking up pennies, they add up. Just this morning, walking around our house, I found .36 that went right into our found money jar.

Keep the change!

You don’t have to just use cash to get into the habit of saving your change from any purchases. If you spend $24.37 at the grocery store, throw the .63 into your found change jar. As your jar gets full, convert it to cash or deposit it into your savings account.

Many banks now have change machines in the lobby. Be careful of using coin machines at grocery stores because the fees can be big. You can sometimes convert your coins into gift cards for the grocery store (then remove that money from your budget to dump into your emergency fund. There are also apps that can do automatic change savings for you.

Pay yourself first!

One way to really make sure you’re putting money into your emergency fund is to have an automated savings deposit the minute you get paid. That way, you never see it, you don’t spend it, and you won’t fret over it as much as if you have to figure it out after you’ve purchased everything else. Even if you’re just putting in $10 a week, pay yourself first, before you pay your bills. You’re likely to never miss it.

Ask for money!

When friends and family ask what you want for your birthday or Christmas, tell them exactly what you’re working towards and that you’d appreciate cash or gift cards.

Use money-saving apps and coupons to help you stockpile money

Phone apps, store apps, manufacturer’s coupons and other money-saving devices are great if you are using them for things you need, not frivolous spending while you are in emergency mode to get your savings funded.

I use these apps with good to decent results. I do, however, make it a habit to NOT spend so much time chasing deals that I waste precious time I could be earning elsewhere.

- Groupon – while I don’t earn money in any fashion with Groupon, I save money on things we may be trying to do as a family and save a little money (which can be redirected into your emergency fund).

- Rakuten (Formerly known as Ebates) – My Rakuten cash back checks typically go right into my grocery slush fund (to be able to take advantage of bulk purchasing deals), but if we were trying to increase our rainy day fund, those checks would go right in the bank every quarter.

- Ibotta – You basically get paid to buy products you’re already buying! Between deals offered through Ibotta by brands looking to get into your pantry and fridge, the percentage back on your general shopping also earns money.

- Grocery Store App – Kroger is my grocery store of choice to do my biggest grocery runs, and their app gives me a weekly freebie and digital coupons to apply to my bill.

- Price book – well, this isn’t an app, but it is a price book that I’ve created to keep track of grocery prices that can help me save loads on shopping trips. You can read more about how I use a price book here.

Sell things

That’s right – if stuff is sitting in your house and is worth an extra $5-10 on eBay or Facebook, sell it – especially if it is no longer bringing you joy! You can check Amazon for books you own that may be worth selling back to them. There are clothing apps and reselling apps out now that allow you to sell directly to a niche market without the hassles of online auctions, too.

Hold a garage sale

Do one with neighbors to help increase interest and workload. Consider an ‘estate sale’ of sorts if you’re really interested in moving out your excess stuff and are willing to part with a lot of it at once. Here are some good tips for a successful garage sale.

Practical Savings Tips

- Grown your own food – save and preserve what you can so you can spend less later

- Bulk grocery shop with friends or family — you save money but don’t have to invest fully. Deposit the savings in your emergency fund.

- Never budget overtime – it goes right into the emergency fund.

- Checking account overflow – if you made it to the next paycheck with something left over, move that into your emergency fund!

- Practice the 52-week savings plan

- Round up — when you’re writing checks, round up to the next whole dollar in your accounting. At the end of the month, move that excess into your emergency fund as you balance your checkbook for the month.

Some final advice…

None of these ideas will give you a $1000 emergency fund overnight. It does take perseverance and a desire to get your family’s finances to a place where replacing a tire doesn’t do your budget in for the whole month. I realize that some of us are living that close to the edge, and this is a regular cycle for you. Maybe these tips will help you free some of your budget up so that you aren’t living there continually.

Don’t get discouraged easily. This takes building and a change of attitude, which you CAN do. It may take six months or more to build your emergency fund to your $500 emergency fund first goal. But celebrate that you did it and then work on the next!

Your thoughts…

I’d love to hear some of the things you’re doing to create a healthy emergency fund for your family. Let me know in the comments below any tips you have that I may not have covered or questions you have about starting!

After work I would empty my wallet of its change (sometimes when I had a few extra dollars I would throw the bills in too, and “throw it” in my bottom very large sock drawer where I really couldn’t “see” how much was accumulating. After a few years when I got ready to retire and move, I emptied my draw and took over $750 to the bank!

Great tips!

I am having $8 a week put into my savings account so a kid can go to 4H camp next year. I also have my bank transfer the ATM charge refunds they give us,put into my savings account automatically. It sounds small but it is slowly growing.

Yes – every little bit counts!